- Mon – Fri: 9:00 AM – 7:00 PM

- (718) 619-8289

- (888) 412-2399

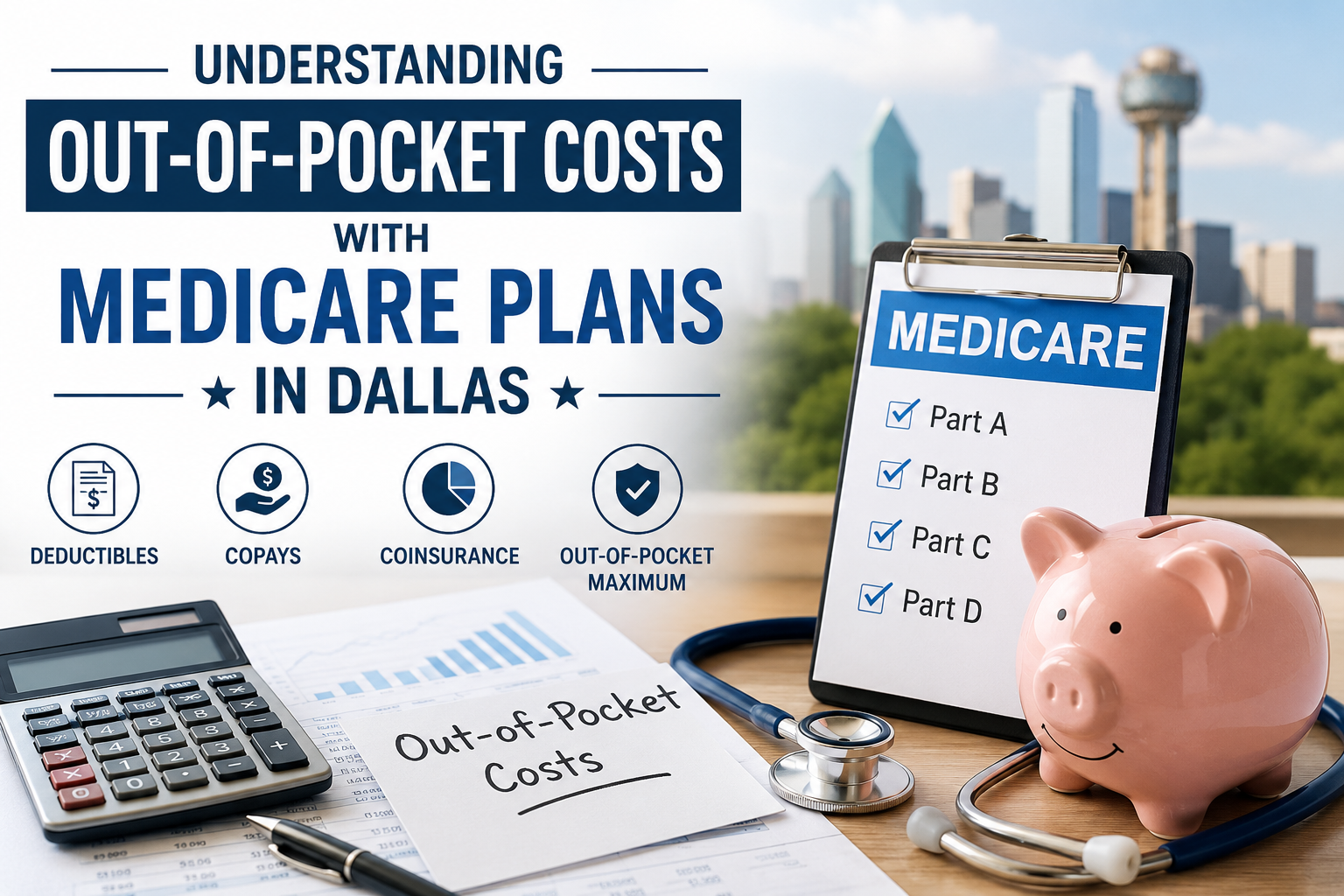

If you are enrolling in Medicare in Dallas, Texas, one of the most important things to understand is out-of-pocket costs and what you may pay beyond your monthly premium.

Many Medicare plans can appear similar at first, but your actual healthcare costs depend on:

• How often you use care

• Which doctors and specialists you see

• Your prescription medications

• How your plan connects with Dallas healthcare system

In Dallas, those differences are often tied closely to:

• UT Southwestern Medical Center

• Baylor Scott & White Health

• Medical City Healthcare

• Texas Health Resources

This guide explains how out-of-pocket costs work so you can compare Medicare plans with more clarity.

These may include:

• Deductibles

• Copays (flat fees for visits or services)

• Coinsurance (a percentage of the cost)

• Prescription drug costs

• Maximum out-of-pocket limits (MOOP)

Understanding how these pieces work together is important when comparing Medicare plans in Dallas.

1. Medicare Advantage Plans (Part C)

Medicare Advantage plans such as HMOs and PPOs often:

• Have lower monthly premiums

• Use copays and coinsurance as you receive care

• Include a maximum out-of-pocket limit for covered medical services

Your costs can vary depending on:

• How often you visit doctors

• Whether you see specialists

• Hospital stays or outpatient procedures

• Whether your providers are in-network

This setup typically includes:

• Medicare Part B premium

• A Medicare Supplement (Medigap) plan

• A standalone Part D prescription drug plan

With this structure:

• Monthly premiums are generally higher

• Out-of-pocket costs when receiving care are often more predictable

• Provider access is typically broader because there are no Medicare Advantage-style provider networks

In Dallas, your out-of-pocket costs are closely tied to provider networks and healthcare systems.

For example:

• A Medicare Advantage plan may structure costs differently depending on whether your doctors are connected to UT Southwestern, Baylor Scott & White, Medical City Healthcare, or Texas Health Resources

• Seeing out-of-network providers in PPO plans can increase your costs

• HMO plans often require staying within one provider network

This is one reason two people with similar Medicare plans can have very different healthcare expenses

HMO Plans

• Require in-network care except for emergencies

• Often use structured copays

• Usually require referrals for specialists

These are common among many Medicare Advantage plans available in Dallas.

• Allow out-of-network care at higher costs

• Offer more flexibility

• Copays and coinsurance can vary depending on where care is received Helpful if your doctors are spread across multiple healthcare systems.

• Designed for individuals who qualify for both Medicare and Medicaid

• Include additional financial support and care coordination

• Available throughout Dallas County for qualifying beneficiaries Some D-SNP plans may also include transportation, dental, vision, and other supplemental benefits.

Copays can vary significantly between plans. If you regularly see specialists affiliated with UT Southwestern, Baylor Scott & White, Medical City Healthcare, or Texas Health Resources, these costs can add up over the course of the year.

Hospital stays, surgeries, imaging, and outpatient procedures often create the largest

differences in healthcare spending.

Examples include:

• Hospital copays

• Outpatient surgery costs

• MRI and imaging costs

• Emergency room visits

These expenses vary significantly between Medicare plans.

Drug coverage can vary based on:• Medication tiers

• Pharmacy networks

• Formularies

Two plans with similar premiums may handle prescription drug costs very differently.

Every Medicare Advantage plan includes a Maximum Out-of-Pocket limit.This is the most you would pay for covered medical services during the year before the plan begins paying covered medical costs for the remainder of the year.

This is one of the most important numbers to compare when reviewing Medicare Advantage plans.

Before choosing a Medicare plan, confirm:

• Is your primary care physician in-network?

• Are your specialists included?

• Does your plan align with your preferred healthcare system?

In Dallas, this often means reviewing access to:

• UT Southwestern Medical Center

• Baylor Scott & White Health

• Medical City Healthcare

• Texas Health Resources

Many residents receive care through Baylor Scott & White, Medical City, and Texas Health providers.

Residents often use specialists throughout Collin County and multiple provider systems.

Many beneficiaries receive care from physicians affiliated with several healthcare systems.

Network participation can vary significantly depending on the Medicare plan.

Many residents rely on specialists connected to UT Southwestern and major Dallas medical groups. Out-of-network care—especially with PPO plans—can increase costs quickly.

Medicare Supplement plans typically work differently than Medicare Advantage plans.

With Medicare Supplement coverage:

• Monthly premiums are generally higher

• Doctor visit costs are often more predictable

• Hospital expenses are usually easier to anticipate

• There are no Medicare Advantage-style provider networks

For Dallas residents who use multiple specialists or travel frequently, this flexibility may be important.

Costs depend on your plan structure, your doctors, your prescriptions, and how often you use healthcare.

Not always. Lower premiums can come with higher copays, coinsurance, and cost-sharing when services are used.

• HMO: Generally, not covered except for emergencies

• PPO: Usually covered at a higher cost

• Medicare Supplement: No network restrictions if the provider accepts Medicare

Once you reach your plan’s annual limit for covered medical services, the plan pays

covered medical expenses for the remainder of the year.

Prescription drug costs are generally tracked separately from medical Maximum Out-ofPocket limits

A Local Perspective Makes the Difference Understanding out-of-pocket costs with Medicare plans in Dallas is not just about comparing numbers—it is about understanding how those numbers connect to:

• Your doctors

• Your prescriptions

• Your hospitals

• Your lifestyle

From Plano to Frisco, McKinney to Richardson, Garland to Irving, and North Dallas to Grand Prairie, your Medicare experience can vary depending on how your plan aligns with providers connected to UT Southwestern, Baylor Scott & White, Medical City Healthcare,

and Texas Health Resources

As your Dallas Medicare insurance advocate, The Popel Insurance Group can help you:

• Review your doctor and prescription list

• Check hospital access (UT Southwestern Medical Ctr, Baylor Scott & White, Medical City Healthcare and Texas Health Resources)

• Compare HMO, PPO, D-SNP, and Medicare Supplement options

• Help you enroll based on your neighborhood and healthcare needs

Call: (888) 412 – 2399